For homeowners seeking to reduce monthly payments, secure a lower interest rate, or tap into home equity, understanding how to refinance mortgage is critical. Refinancing can offer financial flexibility, save money over the long term, and allow you to adjust loan terms to match your evolving needs.

In this comprehensive guide, we’ll break down how to refinance mortgage, explore the types of refinancing, discuss eligibility, walk through the process step-by-step, provide examples, and answer frequently asked questions.

What Is Mortgage Refinancing?

Mortgage refinancing involves replacing your existing home loan with a new one. The new mortgage typically has:

- A different interest rate (often lower)

- Modified loan terms (shorter or longer)

- Potentially cash-out options to access home equity

Refinancing can help homeowners reduce monthly payments, pay off the mortgage faster, or consolidate debt.

Benefits of Refinancing Your Mortgage

Knowing how to refinance mortgage begins with understanding the benefits:

- Lower Interest Rate: Reduces monthly payments and total interest over the loan’s life.

- Shorter Loan Term: Allows you to pay off your home faster and save on interest.

- Cash-Out Refinancing: Access equity for home improvements, debt consolidation, or other expenses.

- Convert Loan Type: Switch from adjustable-rate mortgage (ARM) to fixed-rate mortgage for stability.

- Improve Financial Flexibility: Lower payments free up income for savings or investments.

Types of Mortgage Refinancing

There are several approaches to how to refinance mortgage, depending on your goals:

| Type | Description | Ideal For |

|---|---|---|

| Rate-and-Term Refinance | Change interest rate or term without borrowing additional money | Reduce monthly payments or shorten term |

| Cash-Out Refinance | Borrow extra money against home equity | Home improvements, debt consolidation |

| Streamline Refinance | Simplified refinancing with reduced documentation | Existing government-backed loans (FHA, VA, USDA) |

| Adjustable-to-Fixed Refinance | Switch from ARM to fixed-rate mortgage | Homeowners seeking predictable payments |

Each type serves different needs, and the choice depends on your financial situation.

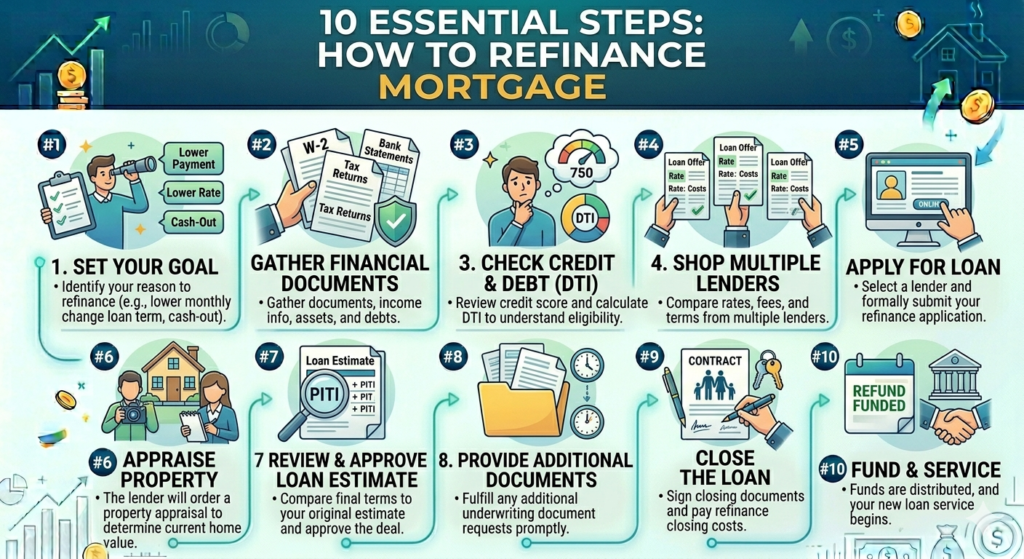

Step 1: Determine If Refinancing Is Right for You

Before learning how to refinance mortgage, evaluate your goals:

- Are interest rates lower than your current rate?

- Do you plan to stay in the home long enough to recoup closing costs?

- Do you want a shorter or longer loan term?

- Are you looking to tap into equity for cash needs?

Answering these questions helps ensure refinancing aligns with your financial goals.

Step 2: Assess Your Home Equity

Your home equity impacts your ability to refinance. Typically, lenders require at least 20% equity for a conventional refinance.

Example:

| Home Value | Current Mortgage | Equity | Eligible Loan Amount |

|---|---|---|---|

| $400,000 | $300,000 | $100,000 (25%) | $320,000 (80% LTV) |

| $500,000 | $400,000 | $100,000 (20%) | $400,000 (80% LTV) |

Higher equity can secure better rates and reduce mortgage insurance costs.

Step 3: Check Your Credit Score

Your credit score heavily influences how to refinance mortgage. Higher scores generally receive lower interest rates.

| Credit Score | Rate Impact |

|---|---|

| 760+ | Best rates |

| 700–759 | Slightly higher rates |

| 650–699 | Higher rates, more scrutiny |

| Below 650 | May require additional documentation or be denied |

Maintaining a strong credit score ensures you qualify for the most favorable refinancing terms.

Step 4: Calculate Costs and Savings

Refinancing involves upfront costs, including:

- Application fee

- Appraisal fee

- Title insurance

- Closing costs (2–5% of loan amount)

Use this formula to estimate break-even point:Break-even months=Monthly SavingsTotal Closing Costs

Example:

| Loan Amount | Current Rate | New Rate | Monthly Savings | Closing Costs | Break-Even |

|---|---|---|---|---|---|

| $300,000 | 6.25% | 5.75% | $150 | $3,000 | 20 months |

If you plan to stay in your home longer than the break-even period, refinancing is likely worthwhile.

Step 5: Shop Around for Lenders

Comparing offers is critical for how to refinance mortgage effectively:

- Check multiple banks, credit unions, and online lenders

- Compare interest rates, closing costs, and fees

- Ask for loan estimates in writing to evaluate total costs

Even a small difference in interest rates can save thousands over the life of your loan.

Step 6: Gather Required Documents

Typical documentation includes:

- Recent pay stubs and W-2s

- Tax returns for the past 2 years

- Bank statements

- Proof of insurance

- Current mortgage statement

Being prepared expedites the refinancing process.

Step 7: Apply for Refinancing

Submit applications to selected lenders. The process includes:

- Pre-approval: Soft credit check for initial rate estimates

- Loan estimate: Written details of interest rate, monthly payments, and costs

- Underwriting: Lender verifies documentation, credit, and home appraisal

Step 8: Appraisal and Inspection

An appraisal confirms the home’s market value, affecting loan eligibility. Some lenders may require inspections to ensure property condition.

| Home Value | Loan-to-Value Ratio | Notes |

|---|---|---|

| $400,000 | 80% | Eligible for conventional refinance |

| $400,000 | 90% | May require mortgage insurance or cash-in |

Step 9: Review and Close

After approval, review the closing disclosure:

- Confirm interest rate, loan term, monthly payment, and closing costs

- Sign loan documents

- Pay closing costs or roll them into the new loan

At closing, the new mortgage replaces the old one.

Step 10: Post-Refinancing Tips

- Monitor statements to ensure correct new payment

- Consider automatic payments to avoid late fees

- Track potential prepayment penalties if paying off early

- Reassess annually to determine if another refinancing opportunity exists

FAQs on How to Refinance Mortgage

Q1: How long does refinancing take?

A1: Typically 30–45 days, depending on lender and documentation.

Q2: Will refinancing affect my credit score?

A2: A hard credit inquiry may temporarily reduce your score by a few points.

Q3: Can I refinance if my credit score is low?

A3: Yes, but interest rates may be higher and approval requirements stricter.

Q4: Should I choose a fixed-rate or adjustable-rate refinance?

A4: Fixed rates provide stability; ARMs can be lower initially but may increase.

Q5: Can I do a cash-out refinance?

A5: Yes, if you have sufficient equity, a cash-out refinance allows you to access funds.

Q6: Are there fees for refinancing?

A6: Yes, including appraisal, title, and closing costs, typically 2–5% of loan amount.

Q7: How much can I save by refinancing?

A7: Savings depend on new rate, remaining term, and monthly payment reduction.

Conclusion

Understanding how to refinance mortgage empowers homeowners to make smart financial decisions. By evaluating goals, comparing lenders, calculating costs, and following the refinancing process, you can reduce payments, secure lower interest rates, or access home equity safely. Refinancing is a powerful tool when approached strategically, aligning with both short-term needs and long-term financial plans.